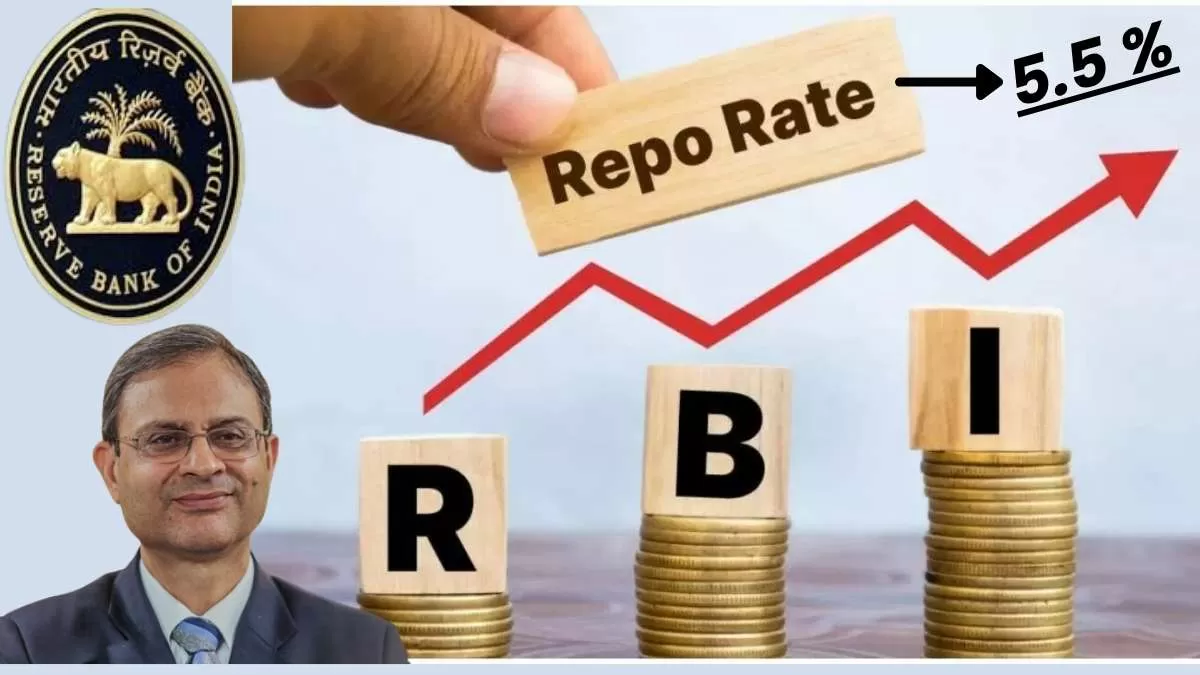

Home loan borrowers can breathe a little easier. In a move that signals relief for households dealing with rising financial burdens, the Reserve Bank of India (RBI) has cut the repo rate by 50 basis points, bringing it down to 5.5%. This is the third reduction in the current year, and for many borrowers, especially those with floating-rate home loans, it spells lower EMIs or shorter loan tenures, depending on how the banks pass on the benefit.

Highlights of Monetary Policy announcement today by Governor, Shri Sanjay Malhotra#RBI #RBIMPC #MonetaryPolicy2025 #rbigovernor pic.twitter.com/I7B43Fm6db

— ReserveBankOfIndia (@RBI) June 6, 2025

But what does this really mean for your pocket? And why did the central bank take this step?

What's the Repo Rate and Why It Matters

The repo rate is the rate at which the RBI lends money to commercial banks. When this rate goes down, banks usually lower their own lending rates. This makes loans—especially home loans—cheaper for the average borrower.

This recent move also came with a 100 basis point reduction in the Cash Reserve Ratio (CRR), allowing banks to free up more funds for lending.

How will a lower Repo Rate impact home loans?

Let’s break it down with a simple example. Suppose you’ve taken a ₹50 lakh home loan for 20 years at an interest rate of 8.5%. Here's what happens after the total 100 basis point cut so far this year:

| Particulars | Before Rate Cut | After 100 bps Cut |

| Monthly EMI | ₹43,391 | ₹40,280 |

| EMI Savings per Month | – | ₹3,111 |

| Total Interest Paid (20 years) | ₹54.14 lakh | ₹46.67 lakh |

| Total Interest Saved | – | ₹7.47 lakh |

Now, if instead of reducing your EMI, you decide to keep it the same and shorten your loan tenure, you could end up repaying the loan in about 17 years instead of 20—and save up to ₹15.44 lakh in total interest!

Why Did the RBI Cut the Repo Rate By 50 Basis Points?

Here are the reasons behind this move:

- Low Inflation: Consumer Price Index (CPI) inflation is comfortably below RBI’s target of 4%. It was 3.34% in March and dipped to 3.16% in April 2025.

- Expected Cooling of Food Prices: According to SBI Research, food inflation is expected to remain well within the target range this quarter, and CPI could even touch 2.9%.

- Slowing Credit Growth: Credit growth dropped from 19.5% last year to 9.8% by mid-May 2025. Meanwhile, bank deposits are growing faster than lending.

- Weaker GDP Outlook: Global trade uncertainties and domestic slowdown have started to affect India’s GDP growth. With inflation stable, the RBI is shifting focus toward growth.

What should you do as a borrower?

Yes. Here’s what you should consider:

If Your Loan is Repo-Linked (EBLR)

- Your bank is likely to pass on the rate cut sooner than later.

- Expect EMI reductions in the next reset cycle.

- You’ll get to choose between lower EMIs or faster loan closure.

💡 Expert Take:

“Most new home loans today are directly linked to the RBI’s repo rate, and that makes rate transmission faster and more transparent,” says Yashish Dahiya, Chairman of PB Fintech.

If You’re on MCLR, Base Rate or BPLR

- Transmission of rate cuts will be slower.

You might continue paying higher rates unless your lender revises them.

Consider switching to a repo-linked loan if your current plan isn’t giving you the benefits.

💬 Santosh Agarwal, CEO of Paisabazaar, notes:

“While the rate cut benefits are real, borrowers on older regimes might not see immediate gains. Check your loan type and talk to your lender about options.”

What Lies Ahead?

SBI’s research suggests the RBI may cut another 25 basis points in the coming months, taking the total cut in FY 2025-26 to 100 basis points. However, that depends on how inflation and economic indicators behave.

Final Word

For homebuyers and existing borrowers, this rate cut is a timely cushion. It reduces repayment burden, makes home loans more accessible, and is expected to boost the real estate sector. If you haven’t yet reviewed your loan details, this might be a good time to reach out to your bank. Whether you reduce your EMI or your loan tenure, the savings are very real.

And in today’s economic climate, every rupee counts.